View

by Phil Bartkowski and Tim Jed

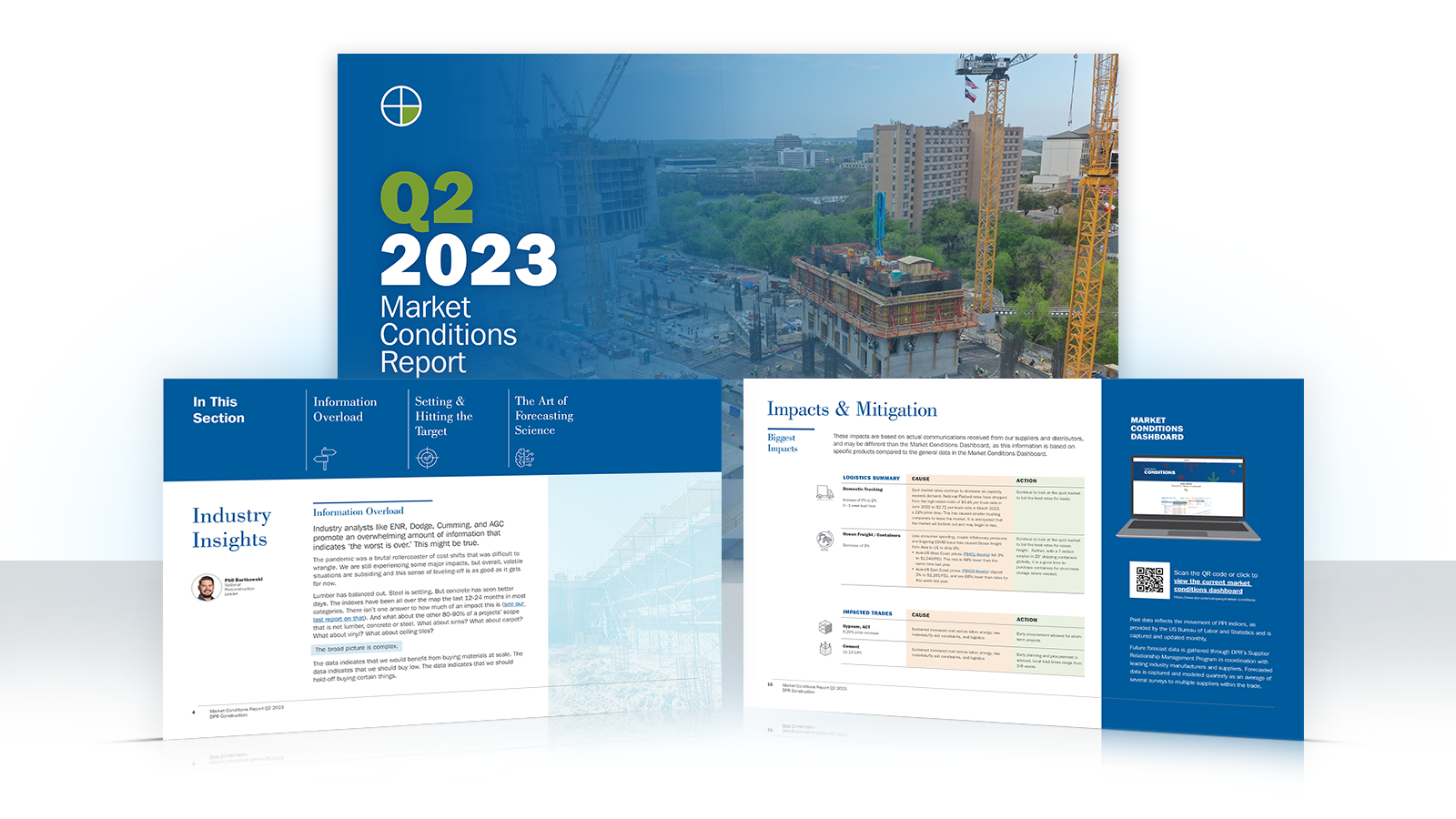

Our Q2 2023 Market Conditions report summarizes current market conditions, industry trends, and mitigation strategies to make more informed business decisions in the quickly changing construction landscape.

Industry analysts like ENR, Dodge, Cumming, and AGC promote an overwhelming amount of information that indicates the worst is over. This might be true.

The pandemic was a brutal rollercoaster of cost shifts that were difficult to wrangle. We are still experiencing some major impacts, but overall, volatile situations are subsiding and this sense of leveling-off is as good as it gets for now.

When it comes to cost, lumber has balanced out. Steel is settling. But concrete has seen better days. The indexes have been all over the map the last 12-24 months in most categories. There isn’t one answer to how much of an impact this is. And what about the other 80-90% of a projects’ scope that is not lumber, concrete or steel. What about sinks? What about carpet? What about vinyl? What about ceiling tiles?

The broad picture is complex.

The data indicates that we would benefit from buying materials at scale. The data indicates that we should buy low. The data indicates that we should hold-off buying certain things.

The data says what it says. Collectively, if the design team, owner and DPR work together, we can consider the data and determine an approach together. If the target is inflexible, it will be more difficult, but not unachievable. If the team accepts the concept of wiggle room on design, cost, and time, then we can collaborate on a plan that can hit our targets.

Over the last two years, we’ve experienced some drastic swings in two key categories related to construction: what things cost and how long it will take. Time and money.

The typical contractual obligation builders face is to deliver a project on time and on budget. Seems like a pretty simple objective, right? In past Market Conditions reports, DPR has discussed how we forecast costs, how we track lead-time issues, and how we monitor labor availability. This scientific, analytical approach is still imperfect.

We continue to hear these questions on a regular basis:

We know our clients and the industry would like a simple answer:

If you’ve come to this report hoping for the answer to these questions, you may be disappointed. We believe a tailored approach is warranted. If we tell our client a number or a date, we should be willing and able to stand behind it.

General trends, graphs and percentages around construction related data are very generic and rarely directly applicable to actual projects.

For example, during the pandemic, when most indicators of future work on the horizon predicted a collapse, we experienced a rise in opportunities and a dramatic strain on key building materials. This, in turn, created such a pressure on cost that the whole industry seemed to be on an escalation red-alert.

The same is applicable right now. Sure, if you look at the major indicators (like we all do), the trend data would indicate we’ve leveled off to a near 0% month to month change according to several construction data trackers out there. But does this take into account the past several years of dramatic rise that got us to this new normal? Should we accept that and run with it?

Data can be extremely reliable, indicative, and valuable when attempting to set a target around time and money.

We do it regularly. Some of the most valuable information that we capture across the projects we build is around what we forecast versus actual outcome. Both from a time and cost perspective, we set out to build reliable and durable targets early, realizing that the first number or date is often the benchmark for all changes moving forward.

We use past data effectively. We look at industry trends and reports. We track supply chain notices and impacts. These things are a piece of the puzzle and should be leveraged.

But this is not ChatGPT. The difference is the practical, personal application of the data; how we take that information and determine how we can relate it, refute it, or use it for this project.

The art side takes as much effort as the scientific approach and the key is to marry those together in a cohesive way to paint an accurate picture. It’s conversational. It’s relational. It’s prospecting. It’s personal. It leverages practical experience to challenge the data and discover the true nature.

Data might tell you that the same building, with the same design, built on a similar site, should be the same cost and built within the same time frame. Though it might be close, it’s not guaranteed.

A period of a few months between those projects could dramatically affect the project’s duration overall due to potential supply chain disruptions. Building just one city or state away from the other project could introduce a completely new set of trade partners that are subject to an entirely different set of local market pressures and production capabilities.

The bottom line is every project is unique, but data alone doesn’t treat them that way. Setting cost and schedule targets is as tailored a process as the project itself.

So what can we do? What can we rely on?

Data & Information:

Candid conversations:

As you review data and begin having candid conversations, consider these questions:

Partner with a builder that will challenge you. Partner with a builder that asks the right questions to understand what you want. Partner with a builder that understands what to expect and is willing to not just report quotes back to you. Partner with a builder that is a collaborator and a steward of your money.

Annual rate of inflation is the lowest since September 2021

Construction employment is up 3.2% YOY

Average hourly earnings are up 6.1% YOY

Despite the recent bank failures and stock declines, optimism remains high in the construction industry.

It will take time to see the longer-term impact of these failures, but in positive news, the inflation rate has now fallen each month since July of 2022, and the annual rate of inflation slowed to 6% from 6.4%— the lowest level since September 2021.1

Due largely to this easing of inflation and shortage of housing, and despite decreased homebuilding sales volumes and lowered prices, homebuilder stocks are outperforming the market.2 Many in the commercial construction industry remain optimistic and believe most segments will improve in 2023, with the exception of lodging, private office, and retail.3

Architectural billings dipped below 50 in November 2022, which was the first time that occurred since February 2021 (a score above 50 indicates an increase in billings, and a score below 50 indicates a decrease in billings). Although they are still below 50, they have been improving since December. The Dodge Momentum Index is echoing this sentiment, indicating anticipated increased construction spending a year out.4

Construction employment for 2022 was up in 40 of the 50 US states,6 and as of February 2023, it is up 3.2% Y/Y and hit a record high 7,918,000, with average hourly earnings up 6.1% to $33.57 craft and office nonsupervisory labor in demand and tight.7 69% of firms expect to increase their headcount over the next 12 months.8

Even as The Washington Post reported The Girl Scouts’ “hotly anticipated new cookie sold out faster than Beyoncé tickets, and wound up on eBay for four times the price,”9 the Global Supply Chain Pressure Index (GSCPI) for February dropped below its historical average for the first time since August 2019.10

Even the number of impacts notices received by DPR (cost and lead time increases) has been steadily falling since September (with an expected tick-up in February, fed by annual notices).

Despite seeing overall improvement to the supply chain, certain products remain problematic with increasing lead times and manufacturers choosing not to quote materials until they are ready to manufacture them.

Semiconductors will continue to be in the discussion regarding the supply chain, and we will likely see continued lead time issues until our supply is shored up to meet the ever-growing demand. Emerging technologies will drive additional demand and time to build infrastructure will make this recovery slow.11

Products related to infrastructure and green initiatives12 will continue to keep demand high, which means continued long lead times and high prices on transformers, generators, switchgear, breakers, metal sockets, and bus plugs. Although copper and aluminum are significantly down, prices have started increasing again. We’ve been told stories of transformers requiring a 174-week lead time at 40% cost premiums, and projects using refurbished short-life transformers to meet commissioning dates, with the assumption that they will need to be replaced within a couple of years after installation.

Glass continues to be an at-risk product due to sand shortages, manufacturing constraints, competing demand from other industries like solar panels and automotive, and hoarding of cullet (broken glass used in recycled glass). French winemakers are seeing issues related to availability of bottles,13 not to be confused by the beer shortage of 2022 which was because of a shortage of carbon dioxide (not bottles).14

Steel is increasing in cost, which is anticipated to be 10% due to seasonal adjustments, inflation, increase interest rates; however, steel producers in Asia are offering lower prices to try to increase volume and regain lost market share. While Russia’s invasion of Ukraine did not start an energy crisis, it affected the crisis significantly. The International Energy Agency (IEA) is calling it “the first truly global energy crisis, with impacts that will be felt for years to come.” It has caused pricing volatility, supply shortages, security issues, and economic uncertainty.15

Bloomberg reported that ocean freight is back to 2018 rates.16 The number of container ships in US coastal waters has fallen to less than half compared to this time last year, indicating a trade slowdown.17

Smaller container ships are being sold for scrap,18 even as the China State Shipbuilding Corporation made delivery on the largest container ship in the world, capable of transporting 24,116 TEU (Twenty-foot Equivalent Units).19

Due to improved snowpack and dredging, the barge traffic slowdown due to drought in the Mississippi river may be coming to an end, but it will take time for things to catch up and normalize.20 The drought in other rivers, like the Rhine,21 and Yangtze22 have not abated, and this will cause continued slowdowns on related barge freight.

In trucking, spot rates for flatbeds are down 14.9% Y/Y, and van spot rates are down 27.0%23 with the average break even price per mile at $2.167.24 Diesel fuel has generally been declining since June 2022, but still 33% above pre-Covid levels ($2.81 v $4.25/gal as of 3/12/22),25 and US crude stockpiles are being rebuilt, and were up 1.2M barrels last week, having risen the last 10 weeks.26

Between January 28 and March 4 of this year, there were 5 train accidents in the US, involving multiple carriers. As we’ve reported in the past, there has been a steady decline in rail service over recent years despite increased profits.

US freight trains grew 25% in length between 2008 and 2017 (up to 3 miles in length) with 67% of trains now arriving on time, down from 85% pre-pandemic, and although the rail strike was averted last December, if there are new requirements to restrict train size or require additional safety standards, rail schedules, deliveries, or costs could be affected.

There were concrete shortages in 48 states last year and costs rose 15% in December of 2022 compared to a year earlier.27 There are many reasons for this, including cement shortages and fly ash shortages (reduction coal fired power plant combustion). Drywall manufactured east of the Rocky Mountains also competes for fly ash, so drywall manufacturers are shifting back to natural gypsum in the east, but this will take several years to fully implement. The President’s announcement to strengthen the “Buy American” requirements during the State of the Union Address could complicate the supply chain for certain products (like concrete) due to the domestic limitations and shortages of raw materials.

The key takeaways, from our perspective: Collaboration, cooperation, and communication continue to be the key to working through the remaining issues in the supply chain.

Here are some of the things we can all do to continue building great things as we partner with our valued customers.

These impacts are based on actual communications received from our suppliers and distributors, and may be different than the Market Conditions Dashboard, as this information is based on specific products compared to the general data in the Market Conditions Dashboard.

| Impact | Cause | Action |

| Domestic Trucking: Increase of 0-2%; 0-1 week lead time |

Spot market rates continue to decrease as capacity exceeds demand. National Flatbed rates have dropped from the high-water mark of $3.45 per truck mile in June 2022 to $2.72 per truck mile in March 2023, a 21% price drop. This has caused smaller trucking companies to leave the market. It is anticipated that the market will bottom out and may begin to rise. | Continue to look at the spot market to bid the best rates for loads |

| Ocean Freight/Containers: Decrease of 3% |

Less consumer spending, couple inflationary pressures and lingering COVID issue has caused Ocean freight from Asia to US to drop 3%.

|

Continue to look at the spot market to bid the best rates for ocean freight. Further, with a 7 million surplus in 20’ shipping containers globally, it is a good time to purchase containers for short-term storage where needed. |

| Gypsum, ACT: 5-20% price increase |

Sustained increased cost across labor, energy, raw materials/fly ash constraints, and logistics | Early procurement advised for short-term projects |

| Cement: Up 10-14% |

Sustained increased cost across labor, energy, raw materials/fly ash constraints, and logistics | Early planning and procurement is advised, local lead times range from 2-6 weeks |

| Pipes, Fittings, Valves: Up 4-24% |

Sustained long lead time and raw material cost | Early procurement advised |

| Capital Mechanical Equipment: Up 18-25% |

Continued increase in demand and shortage of tier 2 components from international suppliers | Early release and procurement advised |

| Transformers, ATS, Water Chillers: Lead time 35-176 weeks |

Continued increase in demand and shortage of tier 2 components from international suppliers | Early release and procurement advised |

While the easing of supply chain issues is positive, DPR has been actively working to control our destiny and prepare for the future in managing our supply chain. Our aim is to ensure a reliable supply chain that keeps our projects on track, hitting critical milestones, and minimizing the effect of outside events.

As suppliers concern over demand and backlog grow, it creates opportunities to secure partnerships with manufacturers who, in stronger demand markets, would not consider selling direct to a general contractor. DPR is actively working with several manufacturers to align and partner with, offering better terms, pricing, and service. Why this matters: The advantage to the suppliers is steadier backlog, and the advantage to DPR and Owners are reduced disruption at better pricing.

With increasing U.S. steel prices, DPR is developing strategic international relationships with producing and processing steel mills to capitalize on competitive pricing opportunities from foreign markets. Why this matters: DPR recognizes current pressures on the domestic steel markets and looks for options that provide better pricing and delivery schedules.

With the recent reductions in freight and trucking costs, DPR has launched a new logistics branch to ensure greater control over transportation scheduling and on-time deliveries. Why this matters: We are now able to receive transportation requests from our front-line teams, move materials, and provide storage close to the project site.

As an enhancement to our supplier quality program, DPR is expanding our qualifications for suppliers to include the Environmental, Social, and Governance (ESG). Why this matters: This will enable us to better understand suppliers and will ensure capabilities in a more holistic manner. A robust quality and qualification program can also enable risk-free international sourcing as a long-term strategy to overcome supply chain issues.

We have seen a recent spike in equipment manufacturers not fulfilling original delivery dates and issuing last minute changes to projects without details on abatement plan nor root cause. Why this matters: DPR was able to leverage our strategic relationships to perform root cause analysis and drive lead time improvements to projects, in some cases reducing delays by up to 18 weeks.

Market remains strong in 2023 but a sense of normalization to pre-pandemic levels is emerging

Learn More

Challenges will continue in 2023 given a difficult debt/equity marketplace and workplace strategy redefinition

Learn More

Recent changes to higher education ecosystem will influence and evolve the student experience

Learn More

Mission critical and advanced manufacturing construction markets continue their growth in 2023

Learn More

Past data reflects the movement of PPI indices, as provided by the US Bureau of Labor and Statistics and is captured and updated monthly.

Future forecast data is gathered through DPR’s Supplier Relationship Management Program in coordination with leading industry manufacturers and suppliers. Forecasted data is captured and modeled quarterly as an average of several surveys to multiple suppliers within the trade.

Download a copy of the report in PDF format.

Information in this report is compiled from third-party reporting that is available to the public. It is not owned by DPR Construction.

United States Census Bureau

United States Department of Labor

United States Energy Information Administration

United States Chamber of Commerce

United States Bureau of Labor Statistics

Engineering News Record

American Institute of Architects

Cumming Corporation

1 https://www.msn.com/en-us/money...

2 https://www.forbes.com/sites/greatspeculations...

3 AGC U.S. Construction Outlook: Rotation or Retreat, March 2023 (Ken Simonson) - AGC 2023 Outlook Survey that included 1032 total respondents

4 https://www.construction.com/n...

5 https://youtu.be/0bgnAn5a2EA

6 AGC U.S. Construction Outlook: Rotation or Retreat, March 2023 (Ken Simonson)

7 AGC Data Digest Vol. 23 No. 9, March 6-10, 2023 (Ken Simonson)

8 AGC U.S. Construction Outlook: Rotation or Retreat, March 2023 (Ken Simonson) - AGC 2023 Outlook Survey that included 1032 total respondents

9 https://www.washingtonpost.com/business/2023/03...

10 https://wolfstreet.com/2023/03...

11 https://fortune.com/2023/03...

12 Electric vehicle and solar products legislation like HR 3684 Infrastructure Investment and Jobs Act; CA CARB rule requiring 100% of new car sales in California to be zero-emission vehicles by 2035 California and is also considering banning all diesel trucks at ports by 2035 with and statewide by 2045 with new vehicles being powered by clean fuels starting in 2024 and other restrictions on high mile diesel trucks in 2025; PG&E’s announcement plans to bury 10,000 miles of power lines in the next decade; The European Green Deal, to reduce greenhouse gas emissions by 55% by 2030 from1990 levels, and become climate neutral by 2050.

13 Global glass shortage hits Washington winemakers (msn.com)

14 U.S. Could Face Another Beer Shortage in 2022 and Higher Prices (marketrealist.com)

15 https://www.weforum.org/agenda/2022/11...

16 https://www.bloomberg.com/news/newsletters/2023-03...

17 https://economictimes.indiatimes.com/small-biz...

18 https://www.hellenicshippingnews.com/ship...

19 https://newatlas.com/marine/msc-tessa...

20 https://kmch.com/2023/03...

21 https://www.bloomberg.com/news/articles/2023-02...

22 https://www.reuters.com/world/china...

23 https://www.dat.com/trendlines

24 https://jbf-consulting.com/breakeven...

25 https://www.eia.gov/petroleum/gasdiesel/

26 U.S. crude stockpiles up 1.2M barrels last week, rising 10th week in row (msn.com)

27 https://www.supplychainbrain.com/blogs...

Photos: Chip Allen

National Preconstruction Leader

Posted on April 12, 2023

Last Updated April 29, 2024